Due to the complex legislation regarding EOTs, a specialist advisor was essential. As our business was a franchise there were additional complications… Hazlewoods were instrumental in clearing the path with HMRC.”

Franchisee

Bayford New Horizons

Bonus payments up to £3,600 per year can be made to all qualifying employees exempt from income tax (but not NICs).

Tax

An employee owned business is solely owned by its employees and can provide a tax-efficient exit route for founding shareholders as well as facilitating succession and improved performance of the business.

Tax can be a complex area to understand. We have the knowledge and expertise to ensure you’re enjoying the tax breaks you’re due, not risking any potential penalties and can guide you through the labyrinth of complex laws. Click here to get in touch.

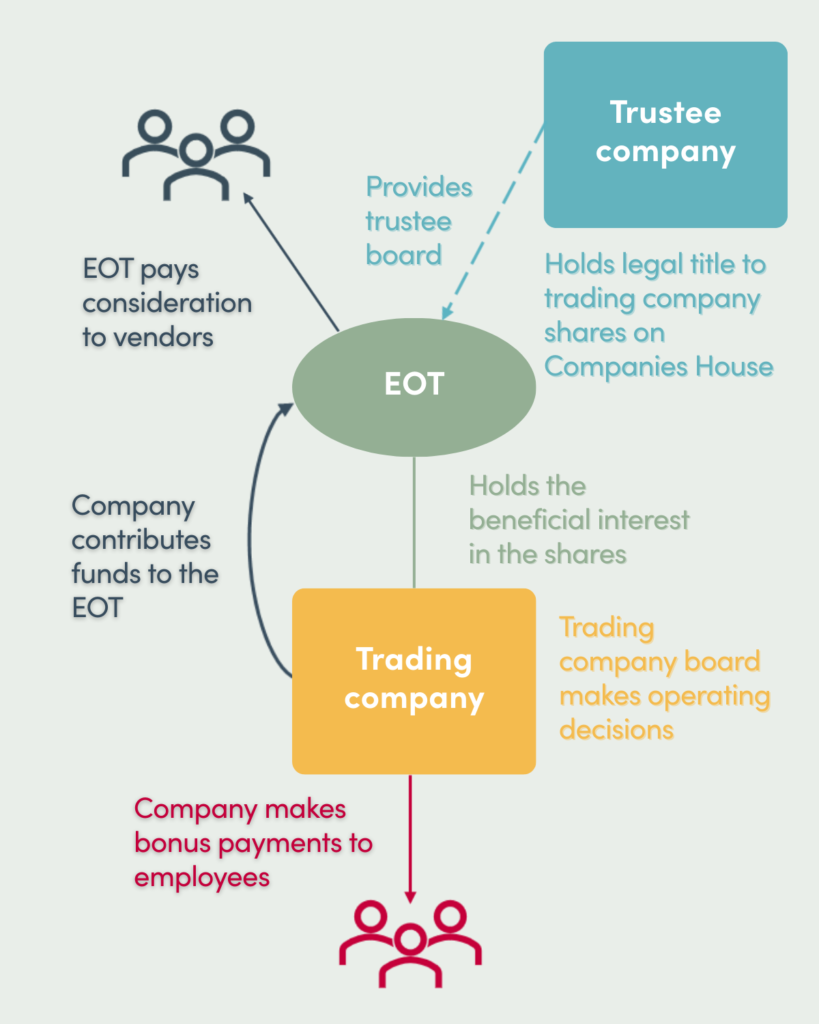

Employee Ownership Trust (EOT) is a government initiative to promote the “John Lewis model”. It involves a special form of trust in which the EOT holds controlling interest in the company on behalf of and for the benefit of the company’s employees so that, in effect, the employees indirectly own the business.

1. Discussion of how the EOT would be put in place and how it would operate going forward.

2. Formal valuation of the company to support the price to be paid for the company by the trustees.

3. Draft a steps paper setting out detailed tax advice relating to the transfer of the company to employee ownership.

4. Legal steps required to enact the transaction and liaise with solicitors and company in respect of transaction documentation.

5. Financial analysis to support the proposed payment schedule.

6. Support the company with the communications to the shareholders and employees where required.

7. Submit clearance to HMRC.

8. Register the trust with HMRC

Due to the complex legislation regarding EOTs, a specialist advisor was essential. As our business was a franchise there were additional complications… Hazlewoods were instrumental in clearing the path with HMRC.”