Is the supported living sector challenging one of investor’s most established assumptions?

For many investors, growth and value creation go hand in hand. The logic is simple: build scale, create efficiencies and improve margins. But what if, in supported living, bigger doesn’t necessarily mean better?

Recent analysis of performance data across a cross-section of supported living providers suggests that the relationship between scale and profitability may be more nuanced than many assume. And for investors, operators and lenders alike, that raises some interesting questions.

Looking beneath the headline numbers

We have analysed performance data from a cross-section of supported living providers, ranging from smaller, owner-managed operators to larger, private equity-backed platforms, including a small number with blended supported living and residential care models.

To enable meaningful comparison, businesses were assessed on a broadly comparable “opco-only” basis using last twelve months’ (LTM) actual performance rather than pro forma or fully adjusted run-rate figures.

While this approach may understate margins for rapidly growing organisations, it arguably provides a more realistic picture of underlying EBITDA (and cash) generation.

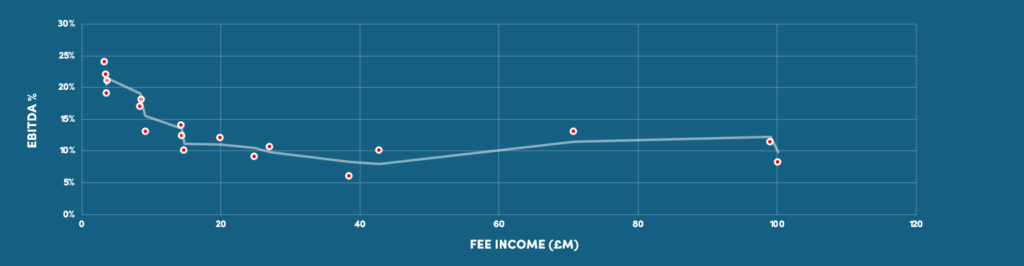

The dataset spans providers with revenues ranging from approximately £3 million to more than £300 million, representing around £826 million of combined revenue.

While this provides a useful snapshot of performance across the sub-sector, it is not intended to represent the whole market and may be influenced by the composition of clients included.

The surprising finding

What the data shows is straightforward: larger providers are not consistently more profitable (at a margin level) than smaller ones.

Average EBITDA margins across the sample sit at around 10.4%. However, beneath that average lies a notable divide.

Providers with revenues below £20 million achieved average EBITDA margins of approximately 14.9%, while those above the £20 million threshold generated margins of just under 10%.

This gap is sufficiently material to challenge the assumption that scaling operations naturally enhances profit margins.

From an investment perspective, this may have a direct implication for how strategies are constructed and executed.

The labour equation doesn’t appear to change

At the heart of the issue is the limited scope for margin expansion through scale. The data shows that direct staff costs, by far the most significant expense line, are tightly clustered at around 69-70% of revenue across the entire sample, irrespective of size.

This suggests that the core economics of care delivery are largely fixed, and that labour efficiencies do not materially improve as organisations grow.

When growth introduces complexity

Instead, the margin compression observed in larger providers points towards the impact of operational complexity. As businesses scale, they typically introduce additional layers of management, central functions and coordination challenges across services.

These factors are not always offset by efficiency gains and can dilute the strong local control that underpins performance in smaller providers.

What does this mean for investors?

For investors, this challenges the traditional reliance on scale-led value creation. The “buy and build” model assumes that growth through acquisition and centralisation will drive margin expansion. In supported living, the data suggests that this assumption does not consistently hold.

This is not to say that larger platforms lack value. Scale can bring diversification of commissioner exposure, improved access to funding and a broader strategic footprint.

However, these benefits appear to come alongside lower margins and therefore cannot be relied upon as a primary driver of financial performance.

As a result, greater emphasis needs to be placed on entry point and asset quality. Acquiring larger platforms at premium multiples without a clear plan to improve operational performance risks embedding structurally lower returns.

By contrast, smaller providers, many of which are owner-managed, demonstrate stronger margins, with the sub-£20m cohort averaging close to 15%. These businesses often benefit from tighter cost control, simpler operating models and closer alignment between leadership and delivery.

A case for more thoughtful consolidation?

The investment opportunity, therefore, is not simply to scale these businesses, but to do so without eroding the characteristics that make them successful.

This requires a shift in focus from financial engineering to operational execution. In a sector where the primary cost base behaves consistently across organisations, returns are driven by granular factors such as workforce planning, service-level performance, pricing discipline and local accountability.

It also suggests a more measured approach to consolidation. Growth in itself is not the issue, but the manner in which it is delivered is critical. Rapid, acquisition-led expansion, particularly where integration is weak, risks introducing complexity faster than it can be controlled, leading to margin dilution. More considered strategies, which preserve local leadership and operational discipline, are more likely to sustain performance over time.

From a portfolio construction perspective, there is merit in balancing scale and efficiency. Larger platforms may offer resilience and strategic positioning, but smaller, higher-margin providers can deliver stronger underlying economics. Combining both can improve overall return profiles, rather than relying solely on scale as the primary value driver.

Final thoughts

Ultimately, the data reinforces a simple but important point: in supported living, size does not dictate success. The approximately five percentage point margin gap between smaller and larger providers is too significant to ignore.

For investors, this means adopting a more disciplined and selective approach; one that prioritises operational quality over headline growth, and recognises that value is created through control rather than scale alone.

If you would like to find out more, please get in touch with one of our health and social care specialists who will be happy to discuss this topic further.