The final version of the Charities Statement of Recommended Practice (SORP) 2026 was published on 31 October 2025, with changes coming into force for periods commencing on or after 1 January 2026. This incorporates the new version of the Financial Reporting Standard (FRS 102). There are several key changes to note:

- Leases

- Revenue recognition

- Trustees Report narrative updates

Leases

As anticipated the changes to accounting for leases adopt the changes brought into the revised FRS 102; you can find more information on this in our Changes in FRS 102 for lease accounting article.

For charities, the following will need careful consideration: Peppercorn and below value leases.

Peppercorn leases

A peppercorn lease is a lease where the annual rent is a nominal or token amount, such as £1. The amount is more ‘symbolic’ rather than reflective of actual money paid for use of the asset. These are more common within not-for-profit entities, than corporate entities.

Under Module 10B of the Charities SORP 2026, a peppercorn lease arrangement is considered to have the legal form of a lease, however with £nil or nominal consideration value, it is not likely to meet the FRS 102 definition of a lease and is therefore a non-exchange transaction.

What does this mean for the accounting?

- Nominal payments are still expensed through the Statement of Financial Activities

- Charities need to measure the benefit that they are receiving i.e. would the charity have purchased the asset if the nominal arrangement had not been made; has the charity been gifted an asset for ongoing use in the delivery of its charitable activities?

- If the arrangement means that an asset is available for a charity to use to carry out its charitable activities, the fair value of the asset needs recognising as a donated right of use asset, in line with SORP module six. The accounting treatment being Debit asset, credit donation income – the amount to be recognised in line with performance related grant accounting treatment, depending on the underlying agreement. Determining the fair value of the ‘gift’ will be crucial and will need to be considered on a case by case basis.

- This would then be depreciated annually, as with other tangible fixed assets.

Below value leases

These are where consideration is paid (above that of a peppercorn rent), but the rent is less than market value. The key difference here is the non-exchange component of the arrangement. The measurement of this non-exchange component will consider lease payments made and, where the incoming resource is an asset, its fair value, or if the incoming resource is a service, the value of the service to the charity.

What does this mean for the accounting?

- The value of the incoming resources from the non-exchange component is recognised as part of the cost of right-of-use asset when resources are received/receivable. Related income is also recognised at the same time, assuming no performance related obligations, which is unlikely here in the context of a lease.

- Ordinarily, the non-exchange component will reflect the difference between market value rent and actual rent paid.

- This would then be depreciated annually, as with other tangible fixed assets.

Revenue recognition

Revenue changes broadly follow what was previously noted in FRS 102, you can find more information on this in our ‘Are you prepared for FRS 102 changes’ article.

There are a few key areas for charities to note here:

- The first step for charities is to consider whether a transaction is an exchange or non-exchange transaction.An exchange transaction is where a charity provides goods or services to a third party under a contract and receives consideration that reflects the value of those goods or services. For example course fees for education services, sale of goods by a museum.Conversely non-exchange transactions are where a charity receives resources without providing anything in equal value in exchange. For example donations or grants without performance – related conditions.

- If an exchange transaction, the five step model introduced by FRS 102 will need to be applied.

- Income such as donations and legacies are unlikely to be affected by these changes as they are non-exchange transactions. Income continues to be recognised when it can be reliably measured.

- Grants may be a key area that could be complex to understand whether they are exchange or non-exchange transactions.

Charity Reporting Tiers

Charities SORP 2026 introduces three tiers for reporting purposes, rather than the current two tiers:

- Tier 1 – Income up to £500,000

- Tier 2 – Income between £500,001 – £15,000,000

- Tier 3 – Income more than £15,000,000

These tiers will have an impact on whether disclosure requirements in the Trustee Report are mandatory or optional.

Trustee Report Changes

A key aim when reviewing the Charities SORP 2019 was to make things simpler for the smallest of charities, as well as adding further clarity in some key areas of narrative reporting.

The main six areas of change brought into Charities SORP 2026 are:

Impact reporting

The largest area of reform within the Trustees’ Report. All charities will now be mandated to report on the impact they have on their direct beneficiaries and the wider society, through the carrying out of their charitable activities. Personal stories are encouraged to add more meaningful reporting.

Volunteer reporting

All charities are mandated to report on how they use volunteers within the business, and the impact that using them has on delivering their objectives. For Tier 2 and Tier 3 charities, the number of volunteers is also needed.

Sustainability reporting

Sustainability reporting is:

- Not mandatory for Tier 1 and 2 charities but is encouraged.

- Mandatory for Tier 3 charities.

A summary of how the charity is monitoring and assessing ESG (Environmental, Social and Governance) requirements is required here, using key performance indicators for example. If the charity is incorporated and falls under large company thresholds, it must also comply with carbon energy requirements.

Reserves

This is not a new area but is something that the Charity SORP body and Charity Commission have been highlighting as something that historically needs improvement. A description of the reserves held, along with a charity’s policy, is required for all sizes, along with an explanation of why a certain amount is held, where applicable. If there are deficits, these must be explained with reference to how they are going to be improved in the future.

Legacies

This is also not a new area but is legacies have been identified as needing additional disclosure for users of the financial statements. Explanations around timing of receipts and use of legacies should be included within the Trustees’ Report

Other changes

Removal of cash flow statement reporting for smaller charities:

Cash flow statements will now only be required for charities with income above £15m, aligning with Tier 3. Although be careful where reporting for incorporated Charities, which also need to consider company size thresholds; if an incorporated charity does not qualify as a small company a cash flow statement is still required under the Companies Act 2006 (two out of the three following thresholds are exceeded: £15m income, £7.5m assets and 50 employees).

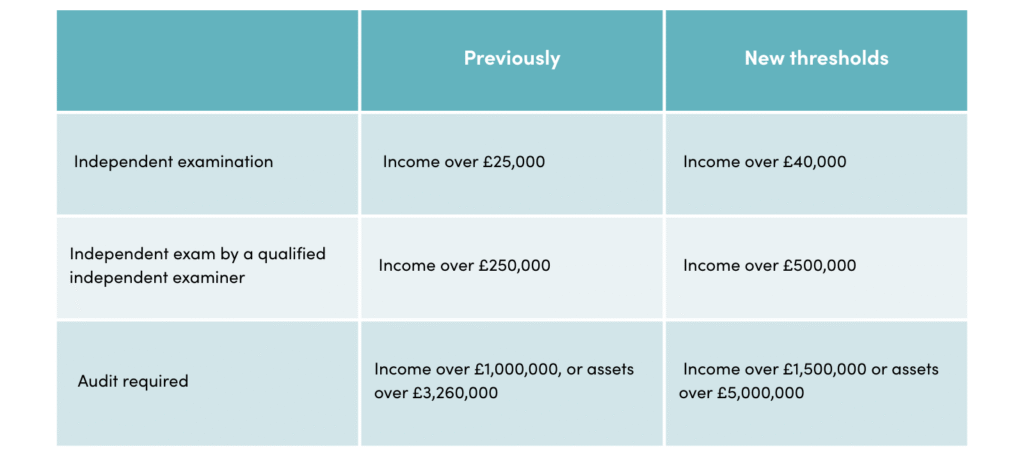

Thresholds for independent scrutiny:

Audit and Independent Examination thresholds have also been reviewed this year, by the Department for Culture, Media and Sport, and are increasing. These changes are anticipated to come into effect from 1 October 2026.

The new thresholds are as follows:

Some of the changes introduced in the Charities SORP 2026 may have a significant impact on your reporting; do reach out to our specialist Charities and Education team who will be able to help you prepare for 2026 reporting requirements.