Further to the Department for Digital, Culture, Media & Sport (“DCMS”) consultation during 2025, DCMS announced significant increases to charity financial thresholds in England and Wales, effective 1 October 2026, with the aim of reducing burdens on smaller charities, raising the audit threshold, alongside increasing limits for independent examinations and accruals accounting.

With the increase in the Charity Audit and Independent Examination thresholds, many charities will move from requiring a full audit to qualifying for an independent examination, or in some cases, not needing an external review at all.

To help you navigate these changes, we have summarised below the key differences between the two levels of scrutiny.

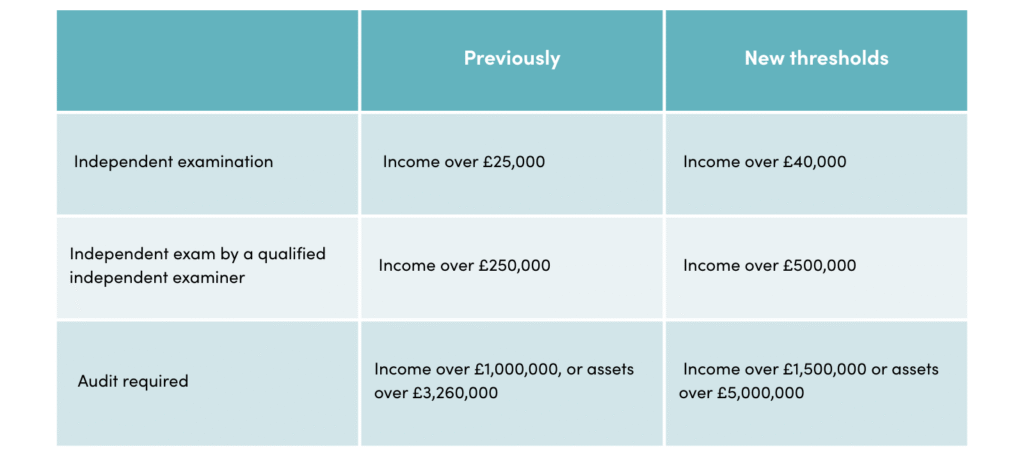

The relevant thresholds are as follows:

Independent Examination

An independent examination provides external scrutiny of a charity’s accounts, offering assurance that they are properly prepared and that the charity is managing its finances responsibly.

Unlike an audit, it does not provide an opinion on whether the accounts present a ‘true and fair view.’ Instead, the examiner reports whether anything has come to their attention that raises concern.

Benefits of an Independent Examination

- Provides a level of independent assurance to the charity’s trustees, supporters and beneficiaries that the charity’s money has been properly accounted for and accounting records kept

- Provides transparency and accountability

- Helps trustees ensure they are meeting their legal and financial responsibilities

What does an Independent Examination involve?

The work that examiners undertake must be in line with the Charities Commission guidance “Independent examination of charity accounts: Directions and guidance for examiners (CC32)”.

As part of a standard independent examination process, the following is expected:

- Check that the charity is eligible to have an independent examination and that there is no conflict of interest that prevents the examiner from carrying out their independent examination

- Perform analytical review of the charity’s incoming resources and expenditure

- Vouch a selection of transactions to third party evidence such as invoices, orders, receipts, payroll reports, etc. to ensure that the transactions are in line with the charity’s objectives

- Check that accounting records are kept to the required standard and that they are consistent with the accounts

- Check the reasonableness of significant estimates and judgements

- Check whether the trustees have made an assessment of the charity’s position as a going concern when approving the accounts

- Ensure that the trustees’ annual report is in line with the accounts

Who can perform an Independent Examination?

Examiners must be independent of the charity and have the skills and experience needed to carry out their responsibilities.

All examiners must have sufficient accounting skills to carry out an Independent Examination and must understand the key governance and reporting requirements that are specific to charities.

The extent of the skills required of the Examiner depends upon the charity’s gross income:

- Income < £500,000, the examiner does not need to be professionally qualified

- Income > £500,000, the examiner must be a member of a recognised professional body (ICAEW, ACCA etc)

Audit

In contrast to an Independent Examination, an audit provides reasonable assurance. It includes an explicit opinion on whether the accounts present a “true and fair view” and comply with accounting standards and legal requirements. A review of the charity’s internal controls and financial systems is also performed as well as an assessment of the risk of fraud.

Benefits of an audit

- Provides a level of independent assurance to the charity’s trustees, supporters and beneficiaries that the charity’s money has been properly accounted for and accounting records kept

- Provides transparency and accountability

- Helps trustees ensure they are meeting their legal and financial responsibilities

- Provides enhanced credibility and builds stakeholder confidence

- May reveal weaknesses in internal controls that are causing inefficiencies

What does an audit involve?

An audit follows the auditing standards from the Financial Reporting Council (FRC). The required work performed is substantially more detailed than that of an independent examination:

- As part of the planning of an audit, the auditor will gain an understanding of the charity’s objectives, operations, internal financial controls and determine the key risks, which then direct the focus of the audit work

- A materiality threshold is determined which in turn establishes the quantity of testing that is required

- An audit will include picking samples of transactions (material as well as random) and agreeing these back to third party evidence such as bank letters, grant agreements, payroll records, contracts, invoices, etc

- Detailed analytical review will be performed on all areas of the accounts and backing evidence will be verified to corroborate this

- Walkthroughs of the internal financial controls will be performed to ensure that they are in line with the charity’s system notes

- Going concern will be assessed in detail and verified to forecasts, budgets as well as reviewed right up to the point of signing

Who can perform an audit?

In the UK, audits can only be carried out by registered statutory auditors. These are individuals or firms authorised and regulated by a recognised professional body (ICAEW, ACCA etc). For charities, the auditor must be properly qualified and registered under UK law to ensure compliance with the Charities Act and Companies Act.

Charities below the thresholds

Non-financial audit requirements

Watch out for when audits are required even though the financial thresholds are not met. Common triggers for an audit can be:

- If the charity’s governing document explicitly requires an audit

- If a grant requires an audit as part of the funding agreement

- If the charity is part of a group, group accounts may need an audit even if the charity itself is below the threshold

Voluntary audits / Independent Examinations

Charities that are below the thresholds can opt to have a voluntary audit / Independent Examination, to gain the benefits outlined above and assist the Trustees in meeting their duties. The six key responsibilities for Trustees (The essential Trustee) are:

- Ensuring public benefit

- Complying with law and the charity’s governing document

- Acting in the charity’s best interest

- Managing resources responsibly, which includes safeguarding and use of the charity’s assets wisely to further its aims

- Act with reasonable care and skill

- Ensure accountability

If voluntary, an independent examination may be more cost-effective than an audit, due requiring less detailed testing than an audit. However, this needs to be balanced against the lower level of assurance obtained by an Independent Examination in contrast to an audit. Both demonstrate financial accountability and transparency.

Summary

The recently published changes to thresholds mean many charities will need to review and reassess their reporting requirements. While independent examinations offer a practical and cost-effective option for smaller charities, audits provide deeper assurance and can strengthen stakeholder confidence. Trustees should review their charity’s size, complexity, and funding obligations to determine which regime they fall under and, if a voluntary scrutiny is opted for, which approach best supports transparency and compliance.

If you’re unsure of next steps for your charity, do reach out to our specialist Charities team who will be able to provide further guidance