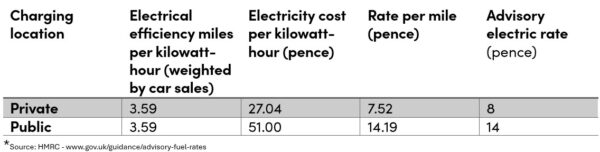

On the 1 September 2025, HM Revenue & Customs (HMRC) issued their latest guidance and updates to their Advisory Fuel Rates as part of their quarterly review. This latest guidance has announced a split rate for electric vehicles (EVs) for home charging and public charging for business travel in company cars. With the latest advice, HMRC have acknowledged the cost disparity between using private and public chargers and therefore they have issued separate advisory electric rates for fully electric vehicles.

This dual-rate system addresses the rising expenses of the public charging network and diversifies the fuel rates system for EV vehicles, while the UK’s EV market continues to expand as the UK looks toward their Net Zero target.

HMRC have also stated that if a charger has been used at a higher cost per mile rate, then you are able to pay at a higher rate per mile as long as you can show that the cost per mile is higher. This evidence could include a receipt. If an employee is paid at a higher rate, taxable benefits will incur if repayment exceeds 14p a mile and these will need to be reported to HMRC either through a BIK on the payroll or on P11d.

It is down to the employer to track whether a vehicle has been charged at a private or public charger. Employers must also update and adapt any in-house policies that reference EV charging to make them relevant to the latest update from HMRC.

It is also important to note that Hybrid cars should be treated as petrol or diesel cars as the above only covers fully electric vehicles. For any Petrol, Diesel, LPG or Hybrid cars, the below will apply.

While the mileage and fuel rate allowances, which covers fuel, wear and tear for privately own vehicles, remains unchanged (See below). A date of review of these figures has not been announced and are not expected to change.