Autumn Budget 2025

The EMI scheme is a tax-advantaged employee share option plan designed to help small and medium-sized businesses attract and retain top talent.

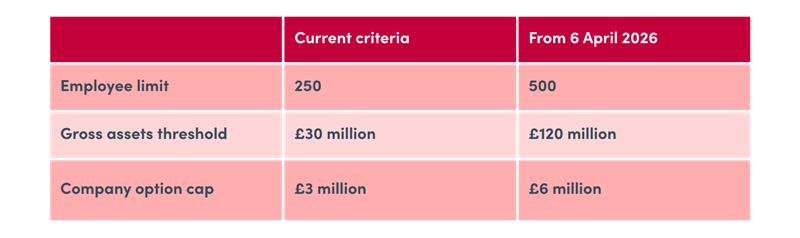

From 6 April 2026, the eligibility for EMI will expand significantly, enabling more start-up and scale-up businesses to benefit from this tax incentive.

Key changes to EMI criteria

Companies can offer EMI share incentives to employees if the following thresholds are not exceeded:

Further enhancement

In addition, the maximum holding period for EMI options is increasing from 10 years to 15 years. This change applies retrospectively to any options in existence that have not already expired or been exercised.

What this means for businesses

These changes will make EMI schemes accessible to a much wider range of companies, including larger businesses and fast-growing scale ups. In turn, employers can better reward their employees, creating a powerful incentive to attract, motivate and retain talent in competitive markets.