Disclosure changes

Whilst Financial Reporting Standard 102 (FRS 102) has been updated for changes in accounting requirements, most notably for leasing and revenue recognition, there are also updated disclosure requirements for small entities preparing their financial statements under FRS 102 Section 1A Small Entities (Section 1A).

The updated disclosure requirements in Section 1A take effect for accounting periods beginning on or after 1 January 2026, and are aimed at giving clarity on disclosures required for financial statements to give a true and fair view.

Additional disclosures include:

- Going concern

- Provisions and contingencies

- Share-based payment transactions

- Current and deferred tax

- Dividends declared and paid or payable

- Leasing arrangements (qualitative and quantitative), short-term leases and low value leases

- Performance obligations in contracts with customers

The latter two items are derived from changes made to FRS 102 in respect of leasing and revenue recognition.

In addition, a small entity is not required under the current version of Section 1A to disclose related party transactions where these had been concluded under normal market conditions. This has been removed in the updated Section 1A, meaning small entities will need to make the same disclosures as those who apply FRS 102 in full, increasing the availability of more sensitive information.

No more ‘filleted’ accounts at Companies House

The Economic Crime and Corporate Transparency Act (the Act) was passed into law in October 2023, providing more transparency on entities registered at Companies House.

As part of this, the Act contains provisions for the removal of the option to file ‘filleted’ accounts at Companies House for small companies and LLPs, to give greater transparency. This has now been confirmed as applying for accounts submitted to Companies House on or after 1 April 2027.

Currently, small companies are able to file ‘filleted’ accounts at Companies House, which are essentially their full set of accounts without a Directors’ report and profit and loss account.

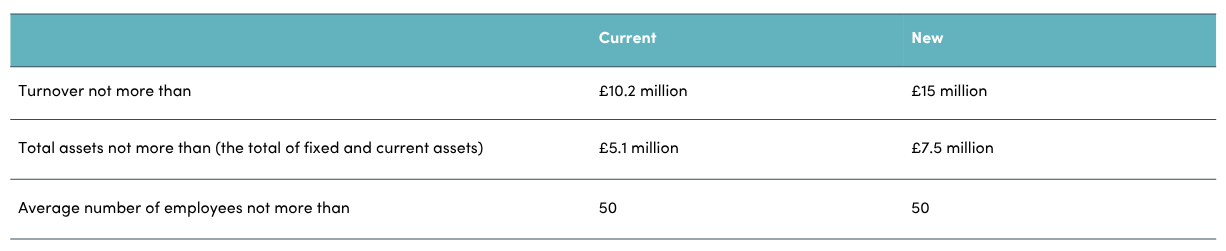

The thresholds used to determine whether a company is small are:

The NEW thresholds are also relevant for LLPs and apply for accounting periods commencing on or after 6 April 2025.

In order to satisfy the size criteria, two out of three of the thresholds must be met for two out of the last three accounting periods. However, a company will not qualify as small if it is ineligible, or is part of an ineligible group.

When assessing size criteria for accounting periods commencing on or after 6 April 2025, the NEW thresholds are treated as always having been in place to prevent any mismatches in assessing the last three accounting periods to determine size qualification.

From 1 April 2027, small companies will be required to file both their profit and loss account and Directors’ report, and so called abridged accounts, which contain a simpler profit and loss account and balance sheet structure, will no longer be an option for small companies to prepare and file.

Directors need to be fully aware of these changes, as the implications of not being able to file ‘filleted’ or abridged accounts are clear.

Many stakeholders, including suppliers, customers and employees, will take a keen interest in the key operating metrics in the profit and loss accounts of small companies, such as turnover, gross profit and profit before tax. There will also be more sensitive matters disclosed, including Directors’ remuneration.

Mandatory software filing of accounts at Companies House

In addition, from 1 April 2027 all companies will be required to file their accounts at Companies House using software only filing with electronic tagging of accounts using iXBRL.

The ability to paper file accounts and to use Companies House web filing service will cease from that date.

If you would like to discuss any of the points included in the article, please get in touch with the team.

Head over to our Audits & Assurance page to see how else we can support you and your business.